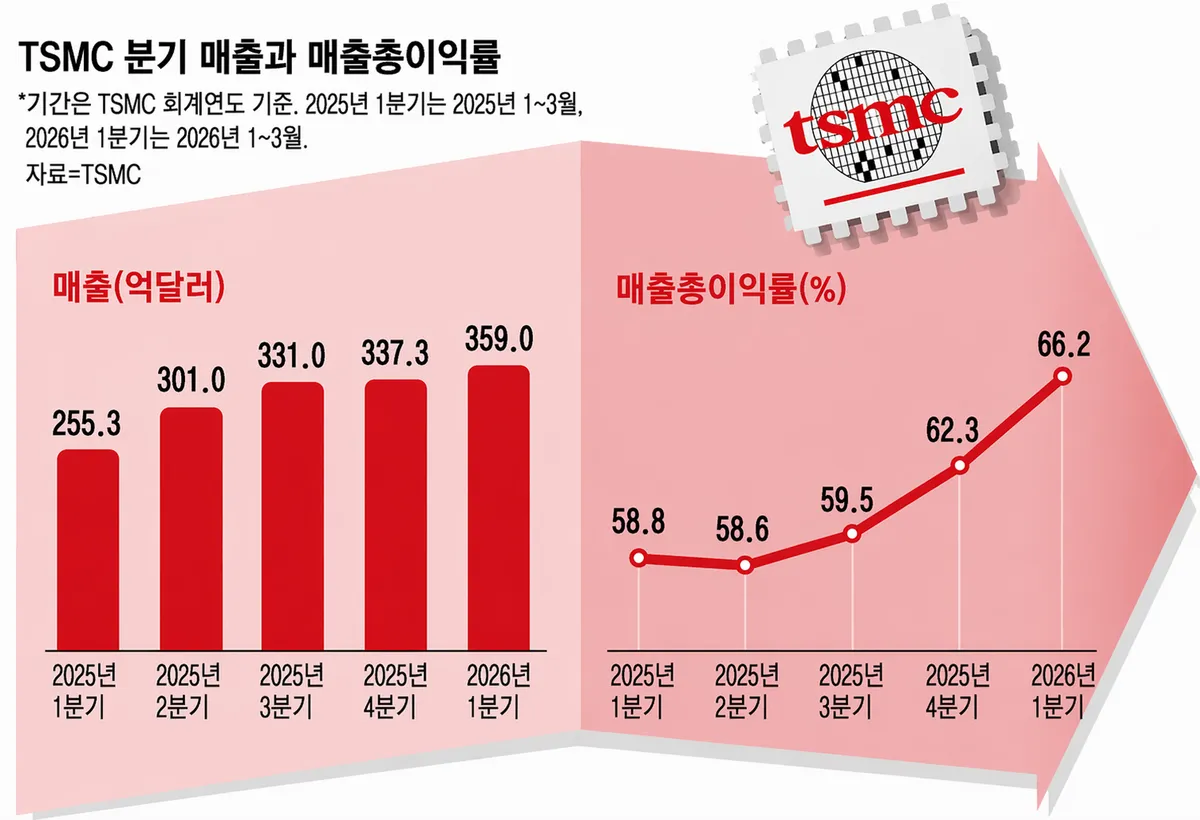

Revenue of $35.9B, gross margin of 66.2% — an earnings beat across the board; full-year 2026 growth outlook raised to above 30%

TSMC (TSM · 2330) reported Q1 2026 results on April 16 (local time) that exceeded market expectations across every metric. Revenue rose 40.6% year-over-year (in USD terms) to $35.9 billion (NT$1.1341 trillion), marking the fourth consecutive quarter of record-high revenue. Net profit surged 58.3% to NT$572.48 billion, while diluted EPS on an ADR basis came in at $3.49, substantially above the consensus estimate of $3.22.

Gross margin reached 66.2%, surpassing the upper end of guidance (65%), while operating margin stood at 58.1% and net margin at 50.5%. Annualized return on equity (ROE) was 40.5%. Despite the earnings beat, shares on the Taiwan Stock Exchange fell approximately 2.6% the following day, as investors took profits following a 31% rally since the start of the year.

Advanced Nodes Running at Full Capacity on AI Demand — 3nm Accounts for 25% of Revenue

The primary growth driver was demand for AI chips. Advanced nodes at 3nm and below accounted for 74% of total wafer revenue, with 3nm representing 25% and 5nm contributing 36%. The High-Performance Computing (HPC) segment — which includes AI and 5G applications — climbed to 61% of total revenue.

AI-related demand is extremely strong. Advances in AI are driving up compute requirements, which in turn are fueling demand for TSMC.

CC Wei, Chairman & CEO of TSMC, earnings conference call

A senior analyst at Counterpoint Research noted that "a sold-out environment — where demand significantly outpaces supply — will remain a defining characteristic of the semiconductor industry throughout 2026."

Full-Year Growth Outlook Raised to 'Above 30%' — Q2 Guidance Also Comes in Above Consensus

Management upgraded its full-year 2026 USD revenue growth outlook from 'around 30%' to 'above 30%.' Q2 guidance calls for revenue of $39.0–$40.2 billion, representing approximately 10% sequential growth and exceeding the market consensus range of $37.0–$38.0 billion. Gross margin guidance for Q2 was set at 65.5–67.5%.

The company indicated that 2026 capital expenditure (CapEx) will be deployed toward the upper end of the previously guided range of $52–$56 billion. Management also disclosed plans for a new N3 fab in Tainan, Taiwan; a second N3 fab each in Arizona, USA, and Japan; and a 2028 timeline for the A14 process node. The 2nm process (N2) is expected to approach company-average gross margins in the second half of 2026.

Middle East Conflict, Helium & Sulfur Supply Chain: 'No Disruptions'

Management also addressed supply chain concerns raised by the Iran conflict. CFO Wendell Huang stated that "specialty chemicals and gases, including helium and hydrogen, are sourced from multiple suppliers across different regions, and we maintain sufficient safety stock." He added that energy supply is being managed stably in coordination with the Taiwan government and state utility providers.

The ADR currently trades at a forward P/E of approximately 24x — a level that some analysts view as discounted relative to the S&P 500 average, given TSMC's AI-driven growth trajectory. The ramp-up of 2nm production in the second half of the year — led by Apple's A20 Pro — is widely cited as the next potential catalyst for the stock.

Data Reference

Based on TSMC's Q1 2026 earnings release (April 16, 2026). Net profit of NT$572.48 billion; ADR diluted EPS of $3.49. Guidance figures are based on the April 16, 2026 earnings conference call.

InteliView Editorial | April 24, 2026