서비스가 새로운 소프트웨어다 — 다음 $1T 회사는 서비스 회사로 위장한 SW 회사

Services: The New Software

원문 보기 (영문) →By Julien Bek. 2026년 3월 5일 발행.

다음 $1조 회사는 서비스 회사로 위장한 소프트웨어 회사일 것이다.

핵심 통찰

모든 AI 도구 창업자가 같은 질문을 한다 — "다음 버전의 Claude가 내 제품을 기능으로 만들면 어떻게 되나?"

맞다, 걱정해야 한다. 도구를 팔면 모델과 경주한다. 그러나 일(work)을 팔면 모델 개선이 곧 서비스를 더 빠르고 싸고 경쟁 어렵게 만든다.

예시: 한 회사가 QuickBooks에 연 $10K, 회계사에 $120K를 쓴다. 다음 전설적 회사는 그냥 장부를 마감해줄 것이다.

Intelligence vs Judgement

- Intelligence(지능): 코드 작성·테스팅·디버깅. 규칙은 복잡해도 규칙이다.

- Judgement(판단): 무엇을 다음에 만들까. 기술 부채를 감수할까. 언제 ship할까. 경험·취향·본능.

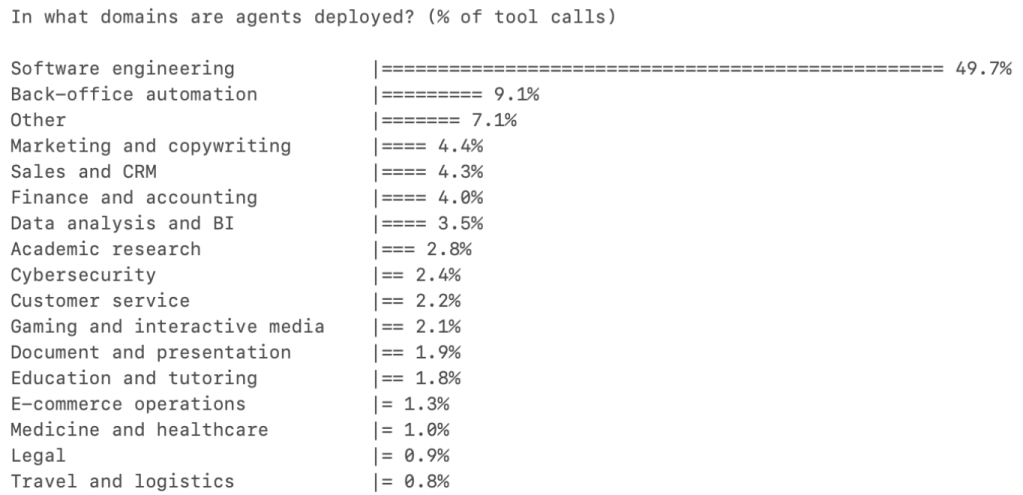

1년 전 Cursor 사용자는 AI를 자동완성으로 썼다. 오늘은 대부분의 태스크가 사람보다 에이전트에 의해 시작된다. 모든 직업의 AI 도구 사용 중 SW 엔지니어링이 절반 이상이다 — 지능 작업이 주를 이루기 때문에 AI가 가장 먼저 임계점을 넘었다.

Copilots vs Autopilots

| Copilot | 도구를 팔아 전문가의 생산성 향상. Harvey(법무 펌), Rogo(IB). |

| Autopilot | 일을 직접 팜. Crosby(NDA가 필요한 회사에, 변호사가 아니라), WithCoverage(CFO에 보험을, 브로커가 아니라). |

어떤 직군이든 일(work) 예산이 도구 예산을 압도한다. Autopilots는 1일 차부터 일 예산을 잡는다.

Autopilot 플레이북 — 아웃소싱을 wedge로

모든 SW $1당 서비스에 $6이 쓰인다. 아웃소싱이 이미 존재하는 곳에서 시작하라:

- 회사가 외부에서 할 수 있는 일이라고 이미 인정함

- 대체할 수 있는 기존 예산 라인이 있음

- 구매자가 책임을 외부에 둘 수 있음

수렴

오늘의 판단이 내일의 지능이 된다. AI 시스템이 각 도메인에서 "좋은 판단"이 무엇인지에 대한 독점 데이터를 축적하면 프론티어가 이동한다. Copilots와 autopilots가 수렴할 것이다. 그러나 시작 포지션이 중요하다 — 이는 autopilots가 어디서 고객을 얻고, 판단까지 처리할 수 있게 할 데이터를 어디서 복리로 쌓을지 결정한다.

Services: The New Software

The next $1T company will be a software company masquerading as a services firm.

Every founder building an AI tool is asking the same question: what happens when the next version of Claude makes my product a feature? They’re right to worry. If you sell the tool, you’re in a race against the model. But if you sell the work, every improvement in the model makes your service faster, cheaper, and harder to compete with. A company might spend $10K a year for QuickBooks and $120K on an accountant to close the books. The next legendary company will just close the books.

Intelligence vs Judgement

Writing code is mostly intelligence. Knowing what to build next is judgement.

Translating a spec into code, testing, debugging: the rules are complex but they are rules. Judgement is different. It requires experience and taste, instinct built on years of practice. Deciding which feature to build next, whether to take on tech debt, when to ship before it’s ready.

A year ago, most Cursor users treated AI as autocomplete. Today, more tasks are started by agents than by humans. Software engineering accounts for over half of all AI tool usage across professions. Every other category is still in single digits. The reason is that software engineering is primarily intelligence work. AI has crossed the threshold where it can do most of the intelligence work autonomously and leave the judgement to humans. Software engineering got there first. It is coming to every single profession.

Copilots and Autopilots

A copilot sells the tool. An autopilot sells the work.

Until recently, AI models were still developing intelligence and judgement, so the right approach was to build a copilot first: put AI in the hands of a professional and let them decide what to do with it. Harvey sells to law firms. Rogo sells to investment banks. The professional is the customer, the tool makes them more productive, and they take responsibility for the output.

Today, the models are intelligent enough that in some categories the best place to start is as an autopilot. Crosby sells to the company that needs an NDA drafted, not to outside counsel. WithCoverage sells to the CFO who needs insurance, not to the broker. The customer is buying the outcome directly. The work budget in any profession dwarfs the tool budget, and autopilots capture the work budget from day one.

The higher the intelligence ratio in any field, the sooner autopilots will win.

The Convergence

Today’s judgement will become tomorrow’s intelligence. As AI systems accumulate proprietary data about what good judgement looks like in their domain, the frontier will shift. Copilots and autopilots will converge. The copilot-to-autopilot transition has already begun in several categories. But the starting position matters because it determines where autopilots can win customers now and begin compounding the data that will eventually let them handle judgement too.

The Autopilot Playbook: Outsourcing as the Wedge

For every dollar spent on software, six are spent on services.

The total addressable market for autopilots is all labour spend in a category, insourced and outsourced combined. But the right place to start is where outsourcing already exists.

If a task is already outsourced, it tells you three things. One, the company has accepted that this work can be done externally. Two, there’s an existing budget line that can be substituted cleanly. Three, the buyer is already purchasing an outcome. Replacing an outsourcing contract with an AI-native services provider is a vendor swap. Replacing headcount is a reorg.

The playbook: companies should start with the outsourced, intelligence-heavy task. Nail distribution. Expand toward the insourced, judgement-heavy work as the AI compounds. The outsourced task is the wedge. The insourced work is the long-term TAM.

Crosby started with NDAs: a well-defined task, primarily intelligence, that most companies already outsource to external counsel. The budget exists, the scope is clear, the ROI is immediate, and the substitution is frictionless.

Opportunity Map

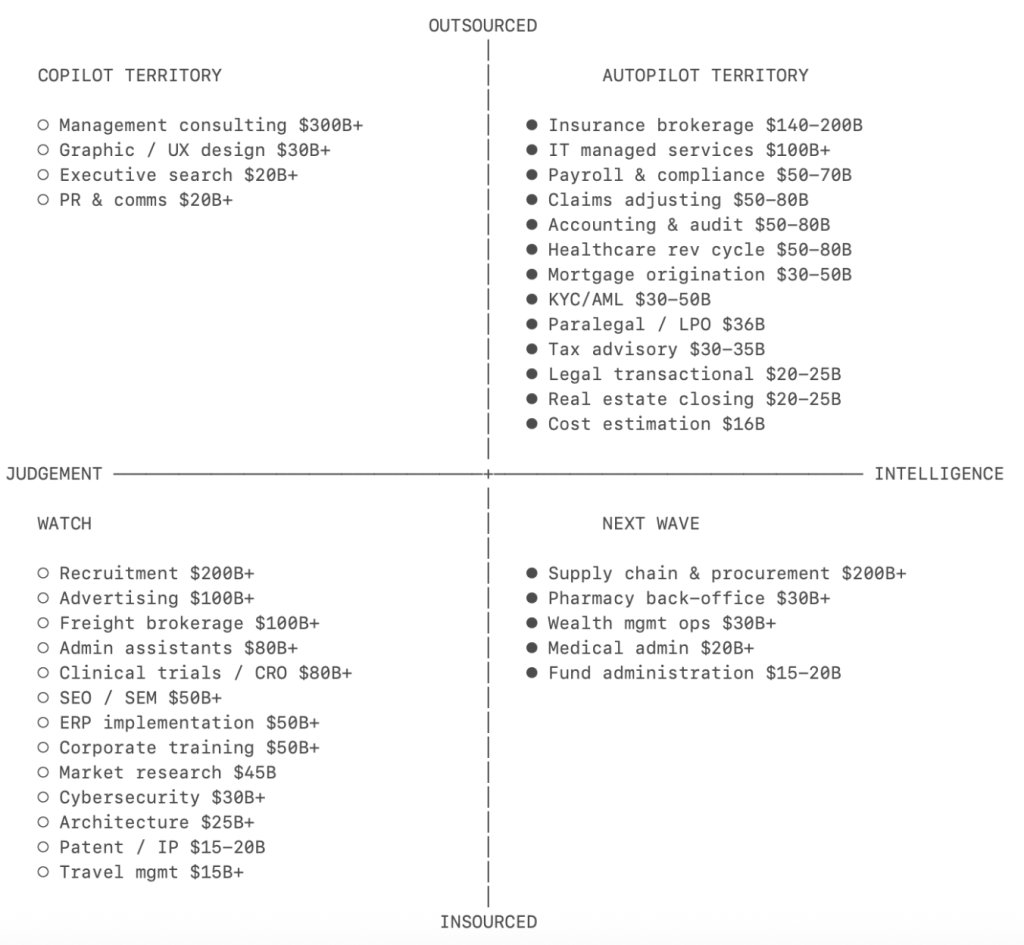

Plotting every services vertical on an intelligence-to-judgement spectrum and outsourced-to-insourced ratio produces a priority map with labour TAM in brackets. The list is illustrative.

Insurance brokerage ($140-200B). The largest dollar market on this list. Standard commercial lines are highly standardised: the broker’s value-add is essentially shopping across carriers and filling forms, pure intelligence work. The distribution layer is incredibly fragmented, tens of thousands of small brokers each running the same process, so no single incumbent controls the customer relationship. WithCoverage and Harper are interesting newcomers.

Accounting and audit ($50-80B outsourced in the US alone). The US has lost roughly 340,000 accountants over five years while demand has grown. 75% of CPAs are nearing retirement, the licensing path is long, and starting salaries lag tech and finance. That structural shortage is pushing firms to accept AI faster than almost any other profession. Rillet is building the AI-native ERP that will close the books. Basis started as a copilot for accountants.

Healthcare revenue cycle ($50-80B outsourced in US). People hear “healthcare” and assume it’s judgement-heavy, but the billing layer is almost pure intelligence. Medical coding is translating clinical notes into ~70,000 standardised ICD-10 codes. The rules are complex but they are rules. The outsourcing is already mature and outcome-based. An autopilot just has to do the same thing at lower cost. Anterior is the furthest along.

Claims adjusting ($50-80B including TPAs). On the other side of the insurance policy, claims adjusting is a separate autopilot surface. Standard-line claims are settled by interpreting policy language against damage schedules and setting reserves using actuarial tables. The adjuster workforce is aging out and nobody’s replacing them. The market is massively outsourced to independents and TPAs like Crawford and Sedgwick. One industry, at least two distinct autopilot opportunities. Pace is building the autopilot for claims handling. Strala is building an AI-native TPA.

Tax advisory ($30-35B). CPA licensing creates a regulatory moat, but 80-90% of the underlying work is intelligence. Every additional jurisdiction a tax autopilot handles deepens its data moat. Multi-jurisdiction complexity is exactly what SMBs outsource because no single in-house accountant can cover it. TaxGPT is an early mover alongside Skalar and Ravical in Europe.

Legal, transactional work ($20-25B). Contract drafting, NDAs, regulatory filings: high intelligence, routinely outsourced. The work product is standardised enough that quality is verifiable, so the buyer can trust AI output without deep legal expertise. Harvey is the emerging leader and is moving quickly to autopilot; Crosby and Lawhive are the autopilot-native newcomers.

IT managed services ($100B+). Every SMB outsources its IT. Patching, monitoring, user provisioning, alert triage: intelligence work running on repeat across thousands of identical environments. The existing software layer (ConnectWise, Datto) sells tools to the MSP. Nobody has yet sold “your IT runs” directly to the company as an outcome. Edra is automating IT processes. Serval is automating IT support.

Supply chain and procurement ($200B+). Most enterprises negotiate seriously with only their top 20% of suppliers. The long tail gets zero attention because it’s not economical to have humans do the work. Contract leakage runs 2-5% of total procurement spend. The wedge is abandoned work: no budget line to justify, no incumbent to displace, just found money. Magentic is building the AI for direct procurement, AskLio for indirect procurement. Tacto is building both the system of record and copilot for the midmarket.

Recruitment and staffing ($200B+). The largest services market on this list. The top of the hiring funnel (screening, matching, outreach) is pure intelligence, but closing a candidate and assessing culture fit is judgement built on years of pattern recognition. The autopilot wedge exists in high-volume, low-judgement roles where matching is standardised. Juicebox, Mercor, Jack & Jill are emerging leaders building across the spectrum.

Management consulting ($300-400B). Huge market but the work is mostly judgement. The interesting question is whether AI can disaggregate consulting into intelligence components (data gathering, benchmarking) and judgement components (strategic recommendations), with the intelligence layer getting automated and the judgement layer staying human. Best candidates TBD.

In 2025, the fastest-growing AI companies were copilots. In 2026, many will try to become autopilots. They have the product and the customer knowledge. But they also face the innovator’s dilemma: selling the work means cutting their own customers out of doing it. That’s the opening for pure-play autopilots.

If you’re building one, reach out. julien@sequoiacap.com / @julienbek

The post Services: The New Software appeared first on Sequoia Capital.