Data center power orders hit $2.4B in Q1 alone, surpassing all of 2025 — backlog surges to $163B

GE Vernova (GEV) delivered a broad-based earnings beat in its Q1 2026 results reported on April 22 (local time). The combination of a dramatic order surge and a full guidance raise prompted multiple investment banks to lift their price targets in the immediate aftermath of the release.

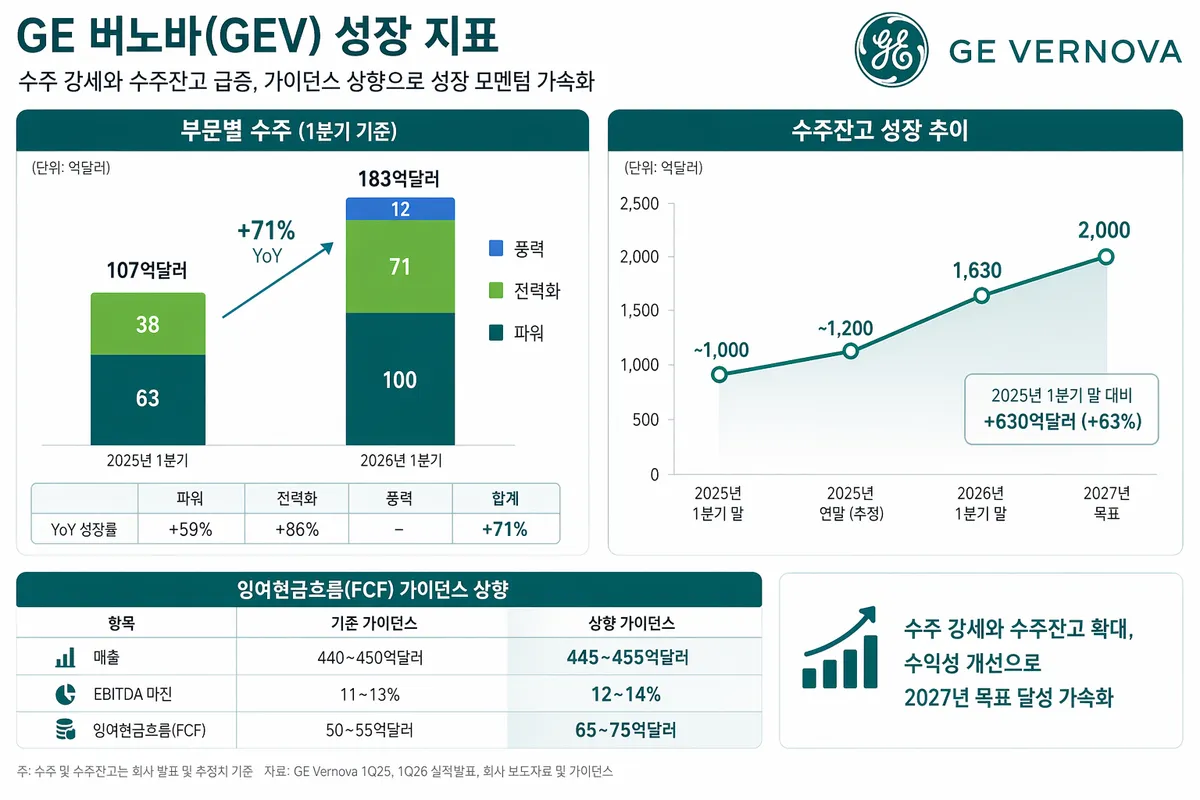

Q1 revenue rose 16.3% year-over-year to $9.34B, topping consensus of $9.27B. Adjusted EPS came in at $2.06, well above the $1.88 estimate. Orders surged 71% YoY to $18.3B, while backlog expanded to $163B (approximately ¥225 trillion).

Data Center Power Orders Hit $2.4B in Q1, Eclipsing Full-Year 2025 Total

The standout line item this quarter was data center-related orders within the Electrification segment. GEV booked $2.4B in data center equipment orders in Q1 alone — surpassing the entire full-year 2025 total in a single quarter. The numbers confirm that AI data center power demand has become the company's primary growth engine.

The Power segment also delivered strong results. Driven by gas turbine price increases and large service contract wins, segment orders grew 59% YoY to $10.0B. Segment EBITDA margin expanded 470 bps to 16.3%. Electrification segment orders surged 86% YoY to $7.1B, fueled by robust North American grid equipment demand.

Wind, however, remained a weak spot. Segment revenue fell 23%, and EBITDA loss widened to $382M from $146M a year ago, driven by tariff headwinds and offshore wind contract losses. Management guided for approximately $400M in full-year Wind EBITDA losses in 2026, though noted that 70% of onshore wind turbine deliveries are back-half weighted, pointing to a second-half recovery.

Full-Year Guidance Raised Across the Board — Free Cash Flow Now Up to $7.5B

Building on Q1 momentum, management raised full-year 2026 guidance across all key metrics. Revenue guidance was lifted from $44–45B to $44.5–45.5B; adjusted EBITDA margin was raised from 11–13% to 12–14%; and free cash flow guidance was increased from $5.0–5.5B to $6.5–7.5B.

We expect to reach $200B in backlog by 2027 — a full year ahead of our prior 2028 target.

Scott Strazik, CEO of GE Vernova

Combined gas turbine backlog and slot reservations are expected to reach at least 110 GW by year-end. The company plans to expand annual production capacity to approximately 20 GW beginning mid-year.

Wall Street Price Targets Lifted Across the Board Post-Earnings

Following the earnings beat, Wall Street analysts moved swiftly to raise price targets. Baird maintained its Outperform rating and raised its target sharply from $1,008 to $1,400; BMO Capital raised from $1,110 to $1,250; J.P. Morgan from $1,000 to $1,150; Oppenheimer from $871 to $1,139; and Citigroup from $779 to $1,110. This followed Redburn Atlantic's double upgrade from Sell to Buy the prior day, underscoring broad and strengthening bullish conviction across the Street.

Data Reference

Based on GE Vernova's Q1 2026 earnings release (April 22, 2026). Backlog of $163B is as of March 31, 2026.

InteliView Editorial | April 24, 2026