Central banks net purchased 1,237 tonnes in 2025. JPMorgan targets $5,000 by year-end; Morgan Stanley targets $5,200.

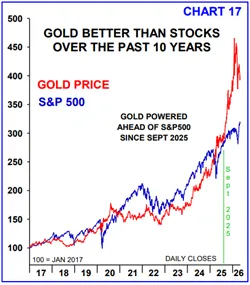

Spot gold is currently trading at approximately $4,730 per ounce. Having surged 55% in 2025 and breaching $4,000 for the first time, the rally has continued into 2026.

Tariff uncertainty, diminishing appeal of U.S. Treasuries, and structural central bank buying are all operating simultaneously.

Russia's 2022 Asset Freeze Changed Everything

The turning point was 2022. When the United States froze Russia's dollar-denominated assets, foreign central banks were jolted. It became clear that the U.S. could freeze any country's assets at will.

Foreign central banks began selling U.S. Treasuries and rotating into gold.

- Prior 10-year average: ~200 tonnes purchased annually

- 2022–2025 annual average: ~1,000 tonnes purchased

- 2025 full year: 1,237 tonnes net purchased

- People's Bank of China official holdings: record 2,309 tonnes in Q1 2026

U.S. Debt Has Become Gold's Fuel — A Vicious Cycle

U.S. federal debt surpassed $36 trillion as of early 2026. The annual fiscal deficit runs at approximately $1.8–2.2 trillion.

The concern is that interest costs on this debt have become the second-largest expenditure item in the U.S. budget, trailing only Social Security.

As foreign investors rapidly dumped Treasuries, the U.S. was effectively pushed toward monetizing its own debt — a dynamic that feeds dollar weakness and inflationary pressure, which in turn stimulates gold demand, creating a vicious cycle.

Moody's recently downgraded the U.S. credit rating, meaning America has now lost its top-tier rating from all three major credit agencies.

Central Banks Buy More on Dips — The Structural Case for a Price Floor

The core of the gold bull thesis lies in central bank buying patterns.

Countries like Poland, which have set gold reserve targets, must continue buying regardless of whether gold is at $4,000 or $5,000. In fact, price dips are viewed as buying opportunities. Unlike hedge funds or retail investors, they do not panic-sell on price declines.

The World Gold Council (WGC) projects central bank purchases of 750–850 tonnes in 2026, providing structural price support.

Central banks buy to meet allocation targets, not price targets. They don't sell on dips — they buy more. This one-directional demand creates a structural price floor.

Wall Street Price Targets — JPMorgan $5,000, Morgan Stanley $5,200

- Morgan Stanley: $5,200 (based on geopolitical tensions and U.S. rate environment)

- JPMorgan Global Research: Expects gold to breach $5,000 in Q4 2026, with long-term potential toward $6,000

- BNP Paribas: $6,000 scenario within the year

JPMorgan expects combined quarterly investor and central bank demand to hold at approximately 585 tonnes.

The Bottom Line

Gold has traditionally been called an asset that 'does nothing' — no interest, no dividends. Yet as the premise of U.S. Treasuries as the risk-free asset comes into question, gold is moving in to fill that role.

With structural central bank buying, the U.S. debt vicious cycle, Middle East geopolitical risk, and dollar weakness all operating in tandem, the argument that "there is more upside ahead" is gaining credibility.