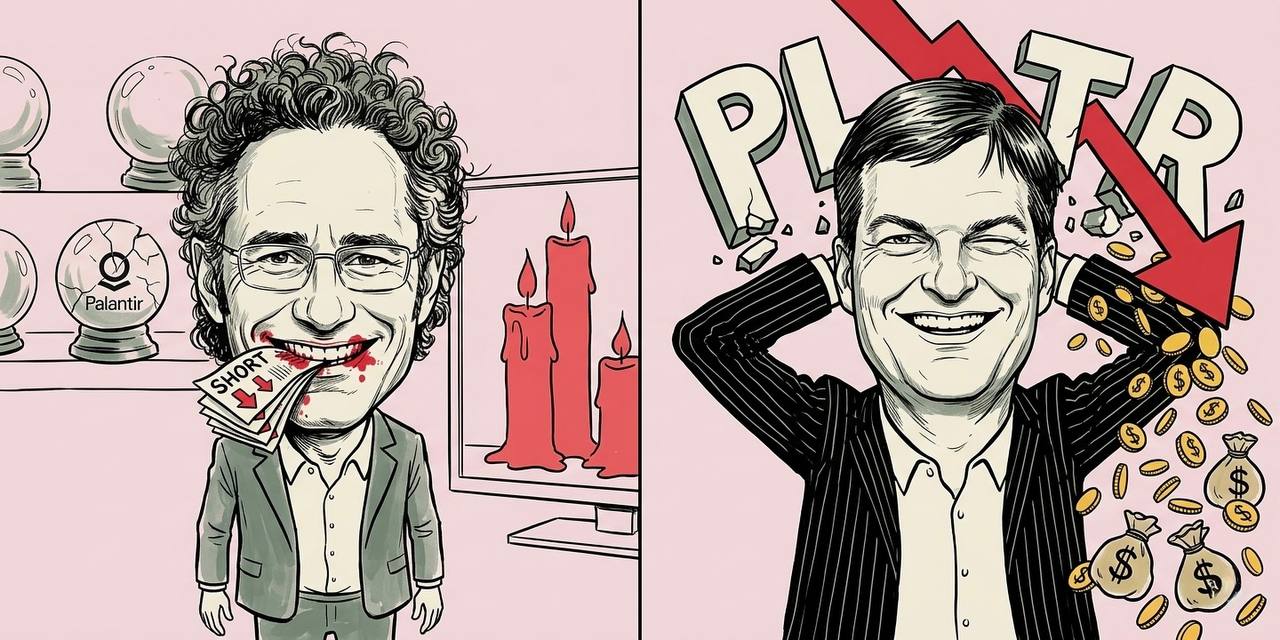

Legendary short-seller Michael Burry has locked onto AI data analytics firm Palantir (PLTR). The real-life protagonist of The Big Short has taken a $9.2M put options position and declared the stock's intrinsic value below $50 — a call that helped send shares tumbling 38% from an intraday high above $207 to the $130 range. Even a public endorsement from President Trump failed to arrest the slide. The Q1 earnings release on May 4 (U.S. time) is shaping up as the first major inflection point.

Anthropic Is Eating Palantir's Lunch

Burry's thesis is blunt and pointed: large language model (LLM) providers, epitomized by Anthropic, are undercutting Palantir's enterprise market with cheaper, faster solutions. When Anthropic launched Claude Managed Agents on April 10, PLTR shares dropped an additional 2%-plus. A broader "SaaS fear" — the idea that AI workflows could be absorbed entirely by LLMs — is weighing on the market.

Burry holds two sets of put options: a December 2026 expiry with a $100 strike and a June 2027 expiry with a $50 strike. The $50 target implies a further 62% decline from current levels. In a post on his Substack, he stated he will not sell a single contract today, reaffirming that Palantir remains severely overvalued.

Valuation metrics partially support his case. The price-to-earnings ratio (P/E) sits at approximately 202x, while the price-to-sales ratio (P/S) based on 2026 consensus revenue estimates stands at 43x. GuruFocus calculates the stock is trading at a 108% premium to fair value. Perhaps more telling is the insider selling activity: executives and insiders have offloaded $432.9M worth of shares over the past three months.

The Smarter the Brain, the More You Need a Nervous System

The bull camp is equally forceful. Wedbush, the Wall Street investment bank, maintains an Outperform rating and has gone on record saying Burry will clearly be proven wrong. Of 26 analysts covering the stock, 15 carry a Strong Buy rating, with an average price target of $198.30 — implying roughly 50% upside from current levels.

The core of the bull thesis is that LLMs and Palantir are complements, not substitutes. The argument: the smarter AI brains become, the more critical the "nervous system" that connects those brains to enterprise data and operational environments. Palantir's operating layer, Apollo, updates hundreds of servers up to 70,000 times per day even in air-gapped edge environments such as battlefields or factory floors — a capability that LLM providers cannot replicate quickly with a simple API call.

The financials provide a powerful shield. Palantir's full-year 2025 revenue came in at $4.475B, up 56% year-over-year. Q4 revenue growth accelerated to 70% — the highest since the company's IPO. U.S. commercial revenue surged 137%. The Rule of 40 metric, which combines revenue growth rate and operating margin, registered 127% — more than triple the industry benchmark of 40%. The company closed 61 contracts valued at over $10M in Q4 alone. One shipbuilder deploying ShipOS for U.S. submarine production cut work-planning time from 160 hours to 10 minutes.

Trump Weighed In — But It Wasn't Enough

On April 10, President Trump posted on Truth Social: "Palantir has proven its incredible warfighting capabilities. Ask our enemies." The public endorsement came as CEO Alex Karp has cultivated close ties with the second Trump administration, helping the company secure a series of new Department of Defense contracts.

Yet even Trump's post failed to reverse the trend. Shares staged a brief intraday bounce before closing the week down 13.7%. Year-to-date losses stand at 26–28%. The market's reaction is widely read as a signal that fundamentals — earnings and valuation — matter more than political messaging.

May 4: The First Answer Arrives

The first decisive test is the Q1 earnings report, scheduled for the early hours of May 5 Korea time (May 4 U.S. time). The Street consensus calls for EPS of $0.22–$0.28, representing roughly 450% growth versus the year-ago figure of $0.04. The company's own 2026 full-year revenue guidance stands at $7.19B, implying 61% YoY growth.

The key metric to watch is U.S. commercial revenue growth. If it holds above 100%, the Anthropic displacement thesis is refuted by the data. If it decelerates into the 50% range, Burry's bear scenario gains meaningful credibility.

Retail investors in Korea should note a critical nuance: Burry's goal is not necessarily for the stock to actually reach $50. His trade profits if fear of that scenario spreads widely enough to move markets. Put options generate gains from volatility expansion alone, even before expiry. Implied volatility (IV) could spike sharply around the earnings release, making risk management around existing positions especially important.

As one Wall Street observer put it: "In the AI era, the first market verdict on whether the brain itself or the infrastructure that embeds that brain in the real world commands a higher premium arrives on May 4."